GP vs LP. What is the difference?

June 24, 2024

If you’ve been around real estate investing the past couple of years, you’ve probably heard the term “real estate syndication.” What does it mean for you as a passive investor?

In this post, we will break down what real estate syndication is and how it works.

So what is a real estate syndication?

In simple terms, a real estate syndication is a legal entity that brings together investors who pull their money to buy an asset to make a profit. Therefore, syndication allows a group of people to participate in an investment that they would not be able to invest in on their own.

Imagine if an asset costs $5M, and 100 people pull money together at $50K each to buy this asset? That’s syndication at its core.

There are different syndication structures depending on the preferences of the general partners, their track record, experience, and the market. As a passive investor, you need to examine the syndication structure, regardless of asset and market class, and ensure that this structure aligns with your investing goals.

Two main types of syndication structures are:

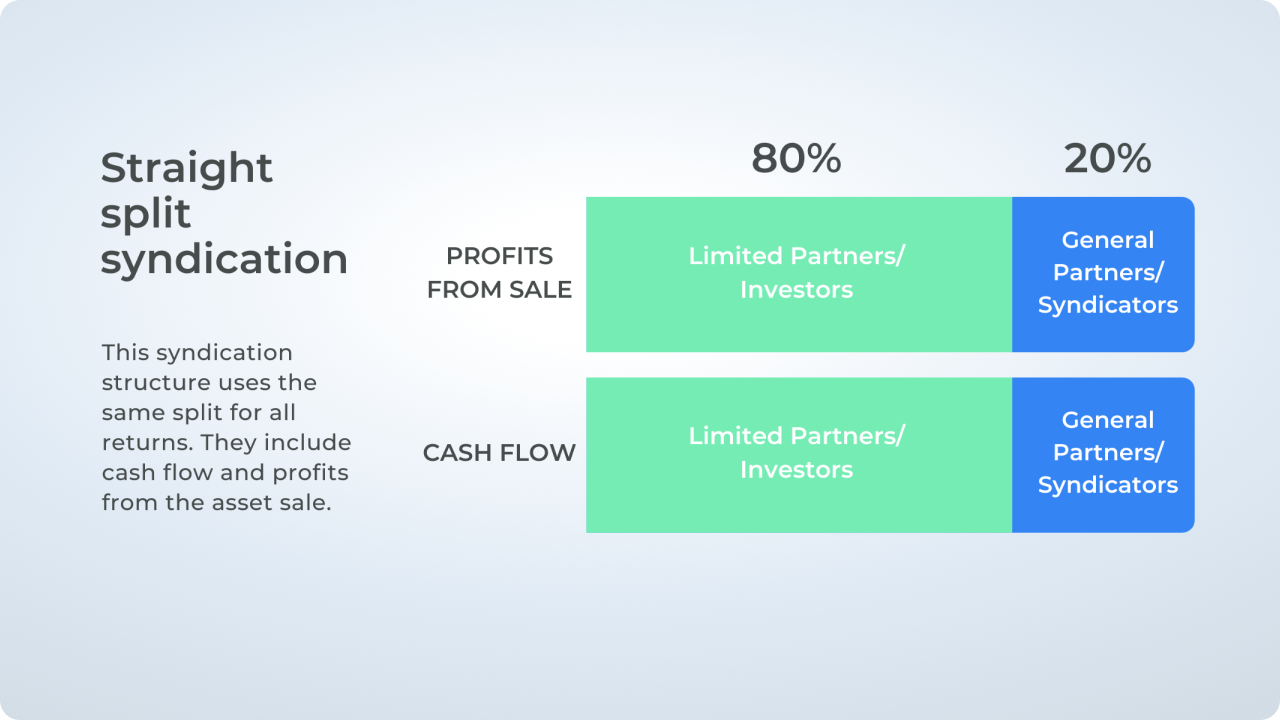

A straight split is the most straightforward structure to understand. It uses the same split for all returns, including cash flow and profits from the asset sale.

Here is a visual example of an 80/20 split.

In this example, 80% of cash flow and profits from the sale go to limited partners or passive investors, and 20% goes to deal sponsors or general partners.

When profits from the asset sale are high, this structure can be especially beneficial for limited partners. For example, on a gain of 40%, a straight split on a $50,000 investment would get you 80% of $20,000 or $16,000.

In a straight split structure, you will likely see fewer benefits from cash flow distributions than with the waterfall structure discussed next. So if you are looking for more ongoing passive income, a straight split might not be for you.

The waterfall syndication structure uses preferred return, and many passive investors love it.

How does it work?

In this structure, investors receive preferred treatment for the first % of the preferred return. For example, you invest $50,000 into syndication with a 7% preferred return, and in the first year, the returns are 7%. It means that you get the full 7% preferred return on your original investment, or $3,500. Deal sponsors don’t get any returns.

The waterfall structure does not guarantee that investors receive the full 7%. However, it ensures that investors get preferred treatment for the first 7% of returns. As a result, deal sponsors are under a lot of pressure to get returns to surpass 7%.

Once deal sponsors reach this threshold, it activates a different % split. For example, any returns between 7% and 14% might be split 70/30 – 70% to passive investors and 30% to deal sponsors. After hitting the 14% threshold, the split changes again. Sometimes to a 50/50.

This structure ensures that deal sponsors take on an asset only if they are confident that it will generate returns above the preferred. Moreover, this structure motivates them to work hard and make the investment perform at its best.

The better it performs, the more returns passive investors get, and the more deal sponsor gets. A waterfall structure is also best if you are looking for a stable source of passive income.

This structure usually brings fewer profits at the sale of the property for passive investors.

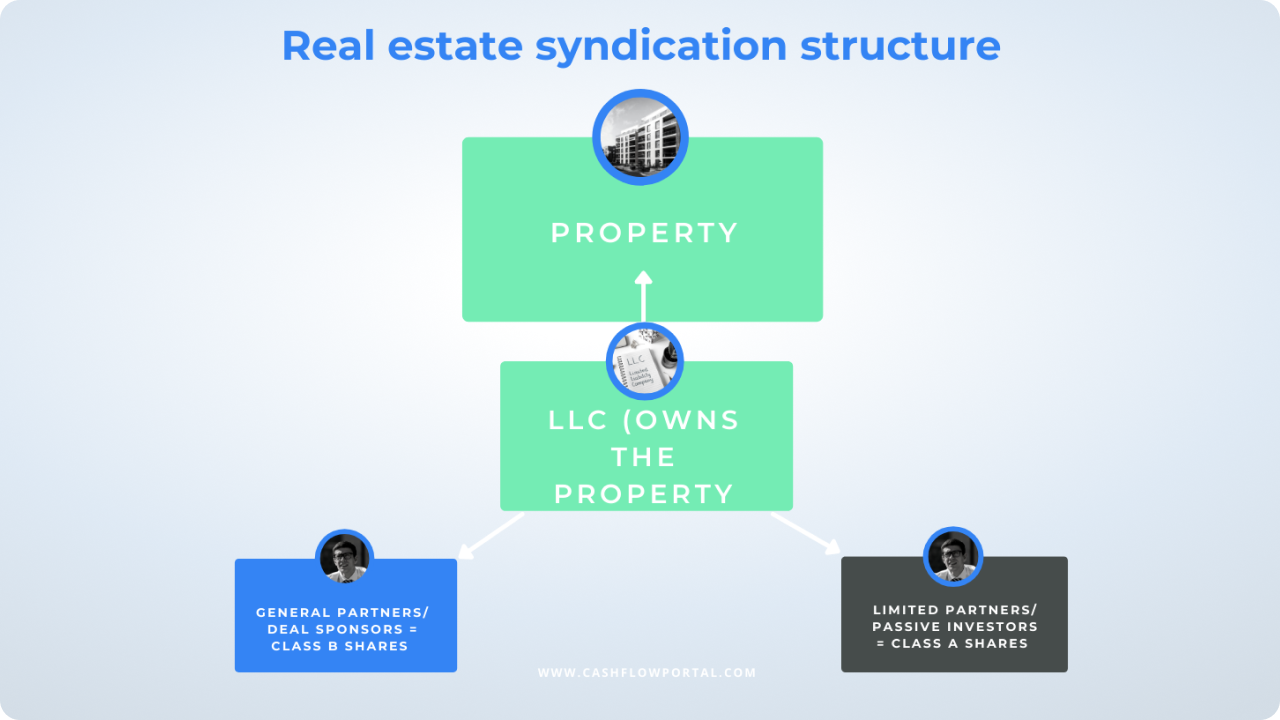

This is how syndications are usually formed:

It’s important to highlight that in real estate syndication, nobody owns the property because an LLC owns it.

The syndicator needs to consider the type of money they are going to raise because it will dictate what type of PPM (private placement memorandum) and other types of documentation they will need when fundraising. Read more about an SEC PPM in this article.

There are usually two SEC rules under which deal sponsors can raise capital:

Usually, the structure of real estate syndications looks like this:

There are two common classes of shares that are sold by the syndication. Usually, you will see:

Deal sponsors invest the sweat equity and are also responsible for investing anywhere from 5% to 20% of the total equity. As a passive investor, you want to see deal sponsors invest substantial equity in the deal.

Some of the advantages of syndication include:

How many years should passive investors expect to have their capital illiquid?

Legally, there are no time limits for syndications. Usually, syndications get sold in 5 to 7 years, so it is a long-term commitment. However, most syndications are sold within three years because once syndicators are confident that they achieved 80% return, they usually sell as it’s challenging to keep doubling your capital in real estate.

On average, passive investors get 6% to 8% in yearly dividends and a 1.8X multiple for their money in five years, including the dividends, which translates into ~50% return over five years.

First of all, this is an unlikely situation because it would take 40% occupancy or less for deal sponsors to fail the mortgage repayment in multifamily real estate. However, in this unlikely event, there are two options:

What happens to passive investors?

Passive investors lose all their investments; however, their personal liability stays intact.

What happens to sponsors?

Deal sponsors are the loan guarantors and usually are unaffected. However, if they misrepresented the information, they will be personally liable for the loan.

Before selecting a deal sponsor, we recommend that you read this article on evaluating a real estate syndicator as a passive investor. In short, there are a few key points you need to look at:

June 24, 2024

December 1, 2022

October 31, 2022