GP vs LP. What is the difference?

June 24, 2024

As individual investors are looking for additional ways to diversify their investment portfolios, many of them turn to real estate syndication. Syndication assumes pooling your capital with the resources of other passive investors to acquire a real estate project together. With such an approach, you can obtain membership in properties that you couldn’t afford to buy on your own.

What determines the success of a syndicated venture is the selected deal structure. Why is that? First and foremost, the structure aligns the interests of all parties and defines how to split the returns between them. Therefore, studying the structure of a property syndication deal you are going to invest in is essential.

In this article, we’ll look at real estate syndication structures from a legal and compensation perspective. We’ll also take a closer look at how these structures influence parties involved in a deal. Armed with that knowledge, you will be able to choose the real estate syndication structure that is right for your investment goals.

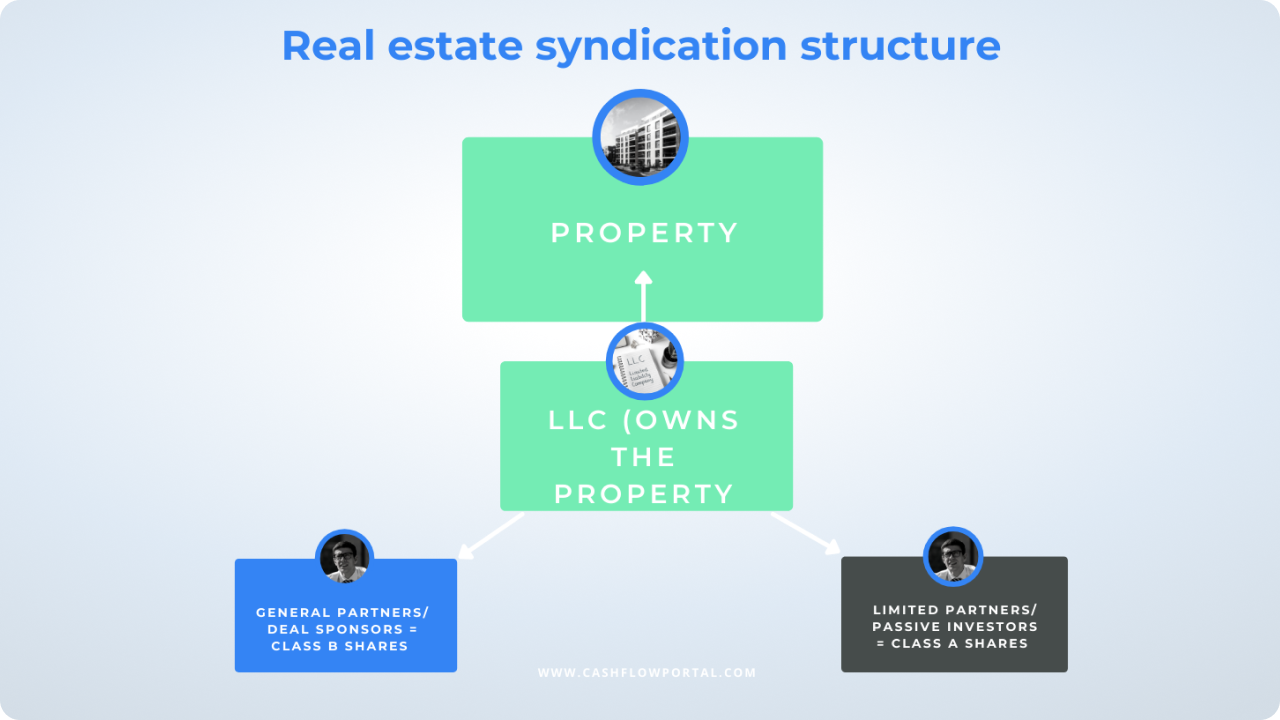

The two parties involved in a real estate syndication deal are:

General partners in real estate syndications are responsible for finding the deal, raising capital, and ensuring the financial motivation for all parties involved. Passive investors pool their funds together to acquire a real estate project and enjoy the returns.

Which role fits you as a real estate investor best? The choice will depend on what you are ready to put in when investing in a property syndication deal. If you prefer a hands-off approach while investing in income-generating assets, the role of a limited partner might be a good option for you. If you feel like your skills and expertise would add to the success of the syndication, consider the role of the sponsor. Check this blog post to discover useful tips for aspiring syndicators.

Now that you know the roles involved in property syndication deals, let’s look through the two common legal entity types used to structure real estate syndication:

With a limited partnership, there are two roles we’ve already covered above — general partners who do all the work and limited partners who invest their funds and aren’t responsible for an entity‘s liabilities. Being a passive investor in a real estate syndication venture structured as a limited partnership, you don’t manage this legal entity. If simply contributing funds does not interest you and would rather prefer more participation in a particular investment deal, then LP might not be the best real estate syndication structure for you.

Unlike limited partners, general partners can be liable for the financial obligations of the legal entity. To minimize this risk, general partners may opt for an LLC creation.

Along with the limited liability of individual members, an LLC features benefits like flexible taxation and relatively low operating costs.

The next important consideration is the specifics of the investment involved in your real estate syndicate, in particular:

First, you need to understand whether you are offering investment security. How do you figure that out?

To adequately protect both general and limited partners, knowing the laws and regulations is a must. When it comes to real estate syndications, the essential federal laws are:

Both of these laws define what an “investment transaction” stands for. Since the concept might be a bit complicated to grasp, a good idea is to attract an asset protection attorney to help you articulate the legal aspects of your syndicate.

Still, there is an easier way to recognize an investment transaction. To make sure that you are offering a security, look for the following characteristics in your business transaction:

Next, when syndicating with different types of investors, real estate syndicators are accountable for different standards and guidelines. There are two types of investors to work with:

Why does the investor type you are working with matter? The type of registration exemption you can file with the Securities and Exchange Commission (SEC) will depend on who you are collaborating with. The type of SEC registration exemption, in turn, will determine further syndication management.

We’ve covered the legal considerations for real estate syndication structures. Now, it’s time to look at the distribution of returns between sponsors and passive investors.

As a rule, limited partners get a return on the funds they contribute to a real estate deal. Deal sponsors lose out to passive investors in capital investments they make and, therefore, the returns earned. To compensate for this gap in earnings, general partners may work fees into a joint venture syndicate. Let’s look through the common fees involved in property syndication projects.

A raise and an acquisition fee aim to compensate for the work done to kickstart the project. Depending on the size of real estate deals initiated, these fees are typically 1-5% of the total capital raised (a raise fee) or the real estate purchase price (an acquisition fee).

An asset management fee aims to compensate general partners for daily project management, property maintenance, and tax or legal costs. The amount of this fee is usually 1-3% of the total capital raised.

A sponsor promote fee serves as an incentive for a general partner. It applies in case a real estate deal brings a return that is higher than expected.

Refinancing is another time-consuming activity that requires attention and due diligence from a sponsor’s side. To compensate for the work performed in this area, general partners may charge syndication members 1-2% of the refinance return.

Selling a property requires certain marketing efforts from a general partner. To compensate for those efforts, a sponsor may charge a disposition fee of 2-3% of the sale price.

Needless to say, the common interest of joint venture syndicate participants is earning returns on the input they make. Therefore, it is essential to set up the compensation structure to agree on the ongoing cash flow distributions and ownership in the syndicate.

Let’s look through the common ownership and compensation structures in real estate syndicates.

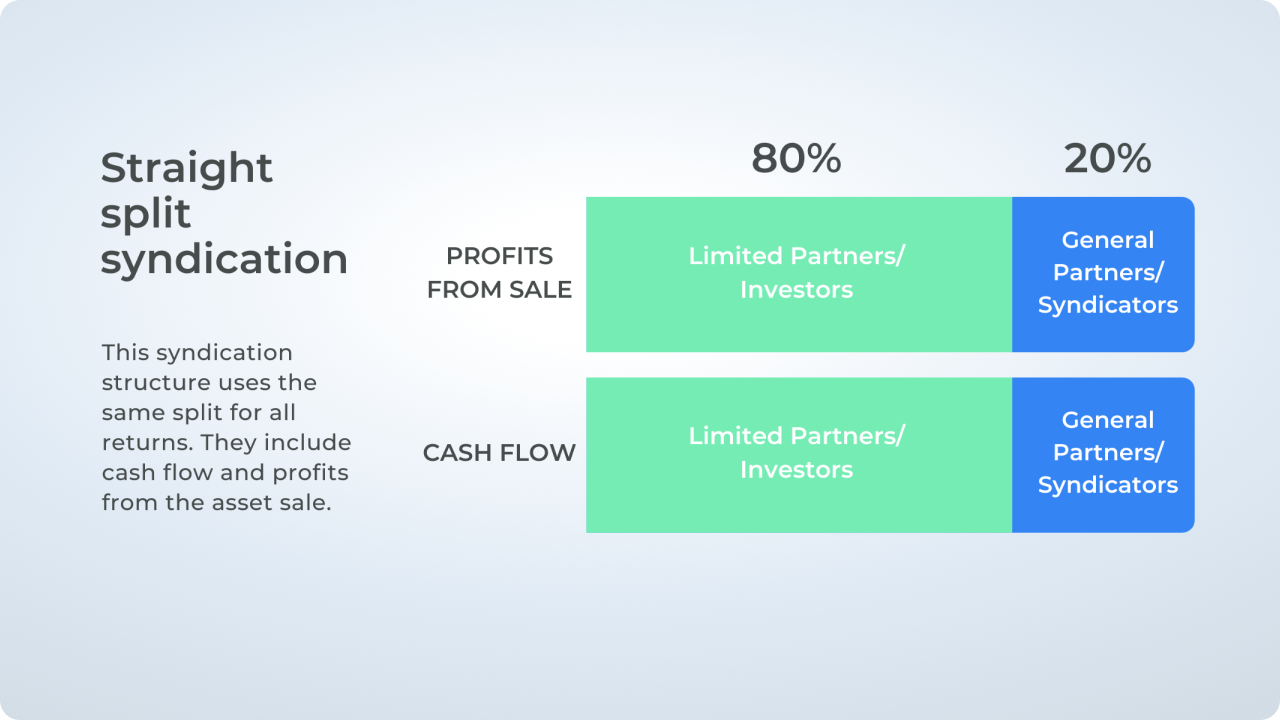

A straight split compensation structure also known as a clean split assumes the distribution of capital gains and cash flow based on the participants’ ownership percentages. Straight split proportions may range from 50/50 to 90/10 share between limited partners and general partners. This real estate syndication structure can be beneficial for limited partners in high-yield real estate investment deals. In certain cases, a general partner may request a larger split share to compensate for the hard work they perform.

With a preferred return compensation structure, passive investors earn a return at a set rate (6-8%) before general partners get any profit. Upon meeting the preferred return threshold, the syndication allocates the remaining compensation with a predetermined payout structure.

A distribution waterfall assumes a more complex real estate syndication structure with a certain financial hierarchy within syndication.

A distribution waterfall structure in a real estate syndication typically involves the following sequential tiers:

Now, what property types can you invest in with real estate syndications to earn passive income? In fact, a variety of asset classes are eligible for real estate syndication: you can invest in commercial real estate or apartment syndication deals.

Let’s outline the common property types that qualify for syndication deals.

Apartment syndication in residential real estate investing covers both single-family homes and multi-family real estate. What makes residential real estate syndications attractive is the steady cash flow from rents. Along with that, apartment buildings are likely to appreciate over time which means attractive profits from the property sale.

Real estate syndications investing in office spaces can also offer attractive returns. Both single-tenanted and multi-tenanted properties provide steady cash flow from rental payments.

With the growing demand for affordable housing, real estate syndications in mobile home parks can be lucrative. This real estate investment type generates strong cash flow as tenants stay in parks for a long time. A mobile home park syndication can either own the park without homes or own both the park and homes in it. In the second case, you leave the property management and maintenance expenses to the tenants.

Engaging with syndication that invests in self-storage real estate is another proven way to generate passive income. Self-storage properties provide storage facilities for individuals to store their household income as well as specialized storage facilities for cars, boats, or documents. This real estate investment option ensures good cash flow and is not labor-intensive in management.

Just like with office spaces, retail real estate syndications invest in both single-tenant and multi-tenant properties. Retail real estate properties include malls, strip centers, power centers, and lifestyle centers, to name a few. The specifics of the retail property syndication subtype are the importance of traffic and parking. For example, for strip centers, vehicle traffic matters most while urban retail properties rely on foot traffic primarily.

As the name suggests, industrial real estate syndications invest in industrial facilities — manufacturing buildings, and R&D facilities. These properties may involve a higher capital investment to prepare specialized facilities required by industrial tenants. Besides, managing and maintaining industrial buildings can be labor-intensive.

Now, you may be wondering: which real estate syndication structure to choose? There is no straightforward answer to this question since many factors matter:

With high profits from the property sale, a straight split real estate syndication structure might work best for you by providing attractive returns. This structure is also good for investment projects with a high potential to appreciate over time. For example, when investing with a self-directed IRA account, your priority is a high profit in the end rather than ongoing cash flow payouts.

If greater cash flow distributions interest you more than earnings accumulated in the long run, the preferred return structure might be a better option for your personal investing goals.

So, you need to assess each real estate syndication deal individually to make sure it aligns with your investment goals. When the motivations of general partners and limited partners coexist harmoniously, the syndicate has a greater chance of achieving the financial goals of all participants.

June 24, 2024

December 1, 2022

October 11, 2022