CRE underwriting. 10 practical tips

June 24, 2024

If you’re here, and if you’ve even thought about real estate investing – congrats! You’re not the only one. It might happen to be a good fit for you. By the end of this article, you will have acquired basic real estate investing skills to put yourself in a position to succeed. What’s more, our real estate syndication software is here to make your journey smoother.

Disclaimer: this does not constitute and investment advice. Please consult your financial advisor before making any investment decisions.

There are many different ways to invest in real estate, including REITs, direct ownership, fix and flip, real estate syndications, etc. In this article, I will be covering just a few of them. As you read, think about which ways suit your personality and needs the best. If you already have a general idea of what you want to get out of real estate investing, use these tips to help give them a more concrete shape. This post will help guide you to the right place when it comes to investing in real estate.

Some of the questions that people who begin their real estate investing journey are:

Read on to find some answers to these questions! Or watch this video if you are a visual learner:

When investing in real estate, my philosophy is rental, long-term whole properties, where you can expect 6%-8% cash on cash return. This return is before you sell the property and can be qualified as dividends. If you include the property sale, you shall expect 10%-15% of annualized return, including cash on cash. As a result, you can double your money every five to seven years.

If you genuinely want to be a real estate investor, you need to understand the importance of sacrifice. If you’re going to be wealthier than others, you can’t play the same game that they do. Therefore, the No 1 rule of real estate investing is sacrifice. Your ability to invest is closely tied to your lifestyle, and your priorities. As a result, if you want to have better returns, you will have to sacrifice some of your lifestyle choices. Like with any other investment, you can also lose money.

The number one reason people invest in real estate is to have the financial freedom to pursue the life they want. For example, when I am 40, I don’t have to work if I want to. I will be able to take my kids to piano practice or a soccer game and spend more quality time with my family and loved ones.

Investing in real estate is a great way to build your net worth. Here is a simple formula that you can use to calculate how much net worth you require to maintain a stable annual disposable income.

In this example, you would need $2.5 million to maintain an annual level of expenses at $100K when you are 40. You can plug in different numbers to customize this formula to fit your situation. Also, note that inflation can make these $2.5 million higher, so you might need anywhere from $3 to $4 million.

Some people achieve their financial goals through investing in stocks and startups, while others do it differently, for example, through real estate investing.

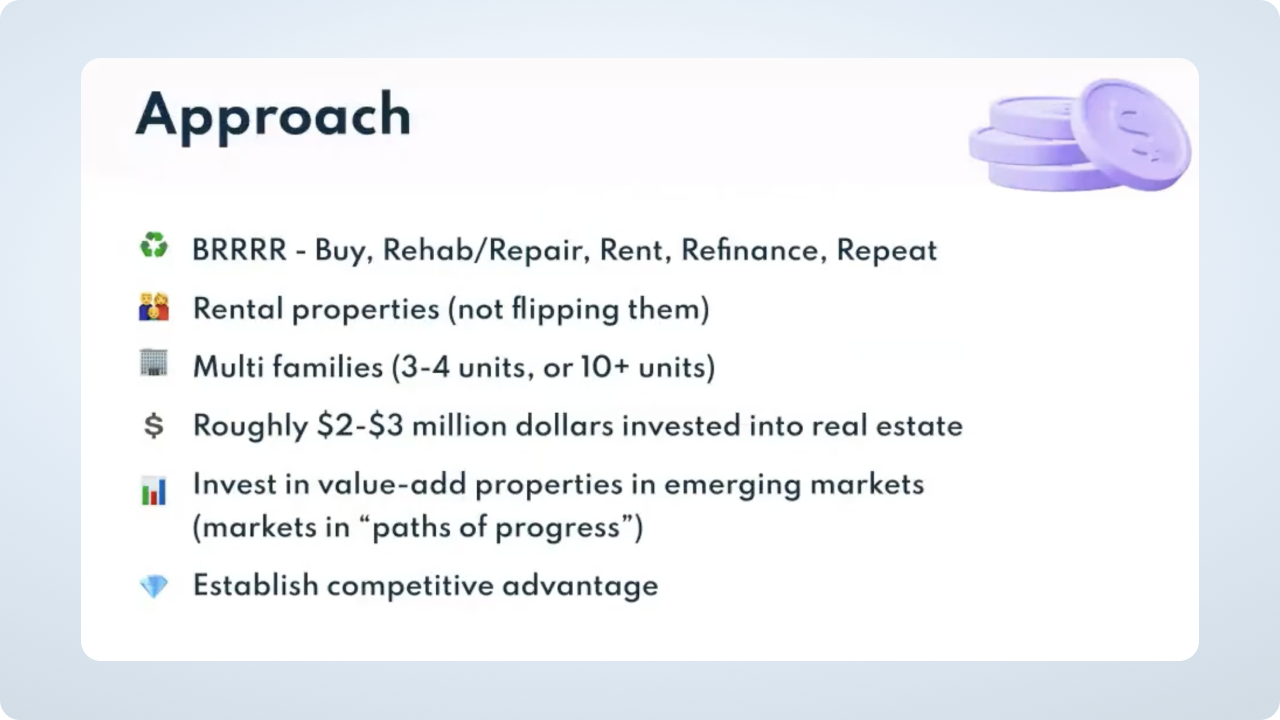

My step-by-step approach is:

There is a term BRRRR, which encompasses this whole cycle. In my case, I buy rental properties but don’t flip them because flipping is a full-time job.

Besides single families, you can also invest in multifamily properties, such as 2-4 units or 10+ units, or even a 100+ unit property. If you are serious about it, you will be putting in $2-$3 million invested into real estate. Then, thanks to the 6%-8% cash on cash return, you get $120K-$140K of disposable income annually generated 100% by the cash flow, not even appreciation.

I invest in value-add properties in emerging markets, including emerging cities and emerging neighborhoods.

To succeed in real estate investing, you need to establish your competitive advantage. My competitive advantage is that I am willing to live with housemates and have a higher-than-average income than lenders like.

Some other competitive advantages include relatives or friends in the area where you aim at buying rental properties. It could also be that you have a spouse that can help you balance the amount of work. Another advantage could be that you are well-versed in Airbnb and have interior design skills. Therefore, before you embark on your real estate investing journey, you need to figure out your competitive advantage.

When it comes to “how,” real estate investing is a business, so your goal is to increase your revenue by increasing rents and lowering your expenses.

The most crucial aspect of running rental properties is property management. It’s essential to have an efficient and reliable system to screen, manage and evict tenants if needed.

Finally, you will need to look for better financing options. It will depend on your income, length of service in your job, etc.

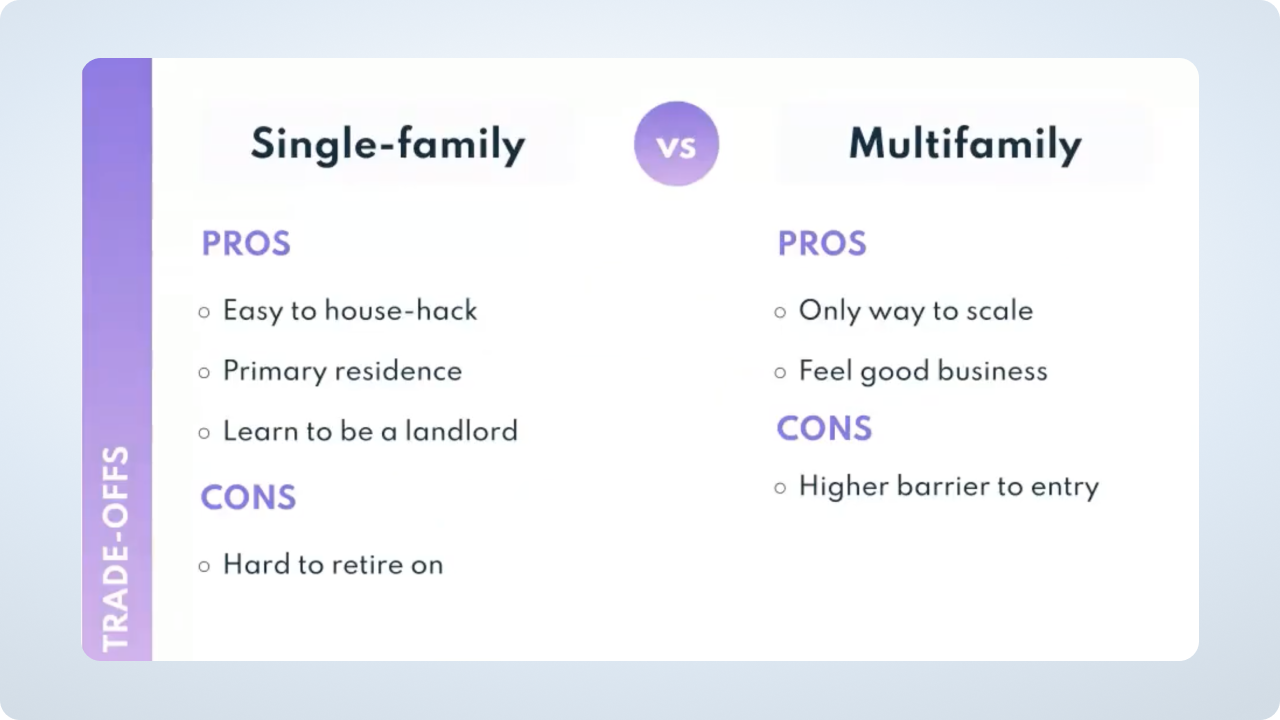

If you are starting out, I recommend buying a single-family property first. It is easy to house-hack, and because you will treat it as your primary residence, you probably will get the best loan terms from the bank with the lowest interest rate and most likely the best leverage. Buying a single-family property is also one of the best ways to learn how to be a landlord.

House hacking means that you buy a house with four rooms and live in one of them while renting out three remaining rooms. You can also house-hack a duplex. For example, you might live on one side of the duplex and rent the other side. Or, instead of renting long-term, you can rent the other side of the duplex through Airbnb.

Most probably, the bank will stop lending you money after buying several single-family homes. Therefore, this type of investment is hard to scale and, as a result, challenging to retire on.

Investing in multifamily real estate is the only way to scale. This investment is also a feel-good business, where you are responsible for the living conditions and the livelihood of hundreds of tenants living on your property.

Multifamily real estate has a high barrier to entry in terms of experience and capital. Also, multifamily properties can be a lot of work and require prior leadership and operational experience as well as good networking skills. If you want to see whether it is for you, first invest in smaller buildings and continue growing your portfolio from there.

By “in-state,” I mean investing in your neighborhood within a one-hour driving radius. If you are starting, I recommend investing in-state with some exceptions. The main advantage of in-state investing is that “what you see is what you get.” You know your neighborhood, right? So you can spot serious bad apples before they get on the bus.

Moreover, because you’re local, you’re more likely to be there for any maintenance issues. Easy access means you get hands-on practical experience of being a landlord. As a result, investing in-state when you are at the beginning of your journey increases your chances for success.

If you don’t have options to invest in-state, you can look for properties out of state. Some of the pros include property prices, as you will have more options to choose from, offering you a lower barrier to entry. For example, if you live in the Bay area, down payments can be as high as $600K+. While out of state, you might find down payments as low as $100K – $150K or even less.

As of my experience, purchasing properties out of state is not worth the effort unless you buy 5-6 homes in the same area. Why? Because you will rely on a property management company that juggles between multiple clients. Some of those clients might have 50 properties with this management company, while you only have one. Therefore, when something goes wrong, the company will prioritize its bigger clients.

As a result, you won’t have much leverage in most cases when it comes to investing out-of-state, and you might need to fly to that neighborhood if you need to check on the property. That one flight will wipe out the next two months of cash flow.

Unless you live in the Bay area, purchase a property within a one-hour driving radius. For example, I live in Seattle, so I would not buy a house in Portland if I could buy it within 45 minutes from Seattle.

If you live in the Bay area, think about moving. I moved from the Bay area to Seattle because of the no state income tax and more affordable real estate. Again, real estate investing is all about making sacrifices.

Considering buying in Sacramento? In this case, you might as well go out of state. Investing in Sacramento vs. investing in Austin is similar because if it takes you 2+ hours to drive to the property, you can get on a plane and get there.

Buying your primary residence should be your main focus in the beginning. Then you can think about purchasing your first rental.

Therefore, if you live in the Bay area and couldn’t buy anything there, don’t let this obstacle stop you. Even if you go out of state to Midwest, purchase your first property. You won’t lose a lot of money and might even break even. However, the experience you will get as a landlord is invaluable for your future investments. And, if you plan to become a syndicator one day, this experience will also help you build your syndication team and pick the right people.

Ready to invest out of state? Here are three types of markets that I recommend:

To give you a more concrete idea, I buy single families in high-appreciating areas because I believe those areas are excellent for living in them. At the same time, I purchase multifamilies in medium appreciation areas, such as Dallas, and I pick landlord-friendly states.

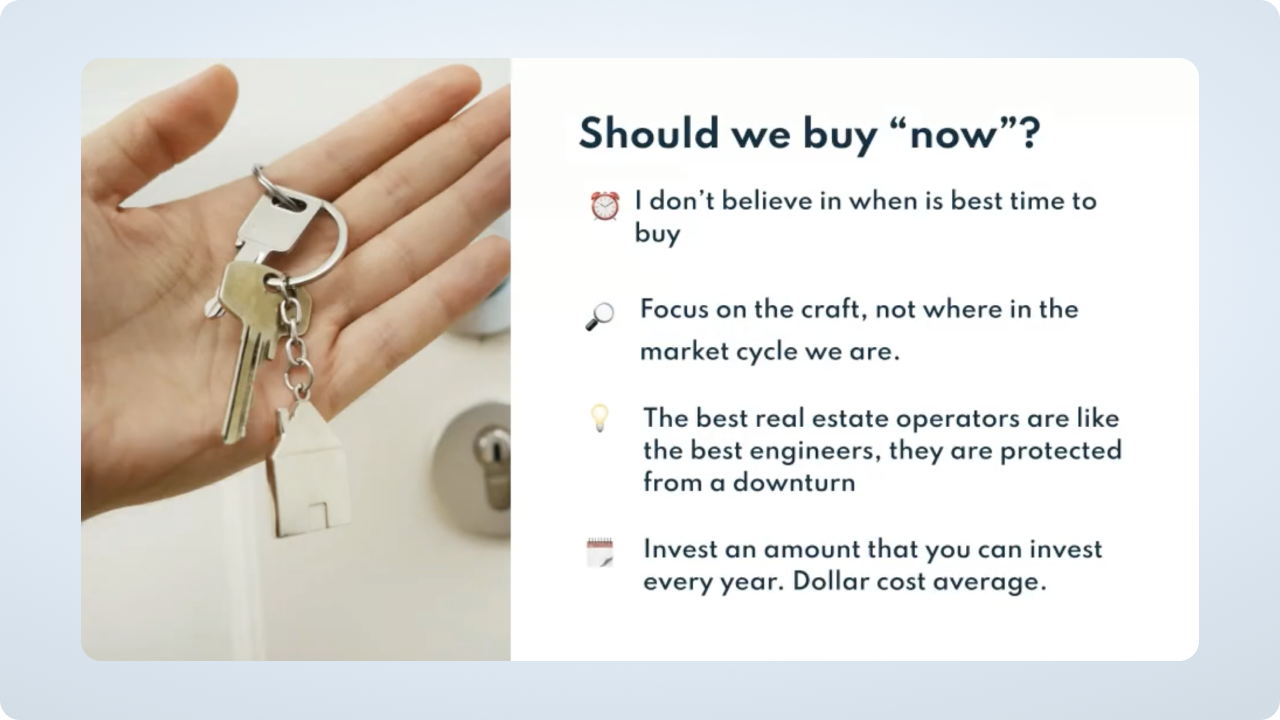

The question I get a lot is “should we buy now?”, “has the market reached its peak, and what if the market drops?” I don’t believe that there is some magical “best time to buy.” When it comes to investing in real estate, you should focus on the craft, not market dynamics.

Similar to the tech industry, in the real estate industry, there are different levels. If you are one of the best real estate investors or one of the best operators, most likely, you will do well. I started over six years ago and now have seven single families, meaning that I buy a house every year, which gives me an excellent dollar cost average.

We got a 0.5% loan brokerage fee in our latest real estate transaction instead of 1%, saving us more than $80K. How did we get this advantage? Because our cabinets for this multifamily property are imported from China directly. Therefore, we are paying 80 cents on a dollar for them.

We have the lowest cost and the most reliable contractors who do the renovation because we’ve done our due diligence and filtered out unreliable contractors with higher than average pricing. Like with contractors, we get the best deals with every vendor. So if we can do everything with the cost of 80 cents on a dollar, we don’t mind paying a little bit more.

The goal is not to maximize globally by finding the perfect timing in the market. But to maximize locally, so even if the entire market is down, you are one of the least affected.

When the stock market went down in 2020, I was not affected at all. Everyone was paying on time. On the one hand, I got lucky because we have the right system of screening our tenants. On the other, the rents were way below the market, and the tenants could afford to pay them. Moreover, my tenants have stable jobs and pass the income and credit score checks. As a result, not even a single tenant has skipped a rent payment in my single-families in Seattle.

Have proper systems in place, and you won’t have to worry about the market and if this is the right time to buy. It doesn’t mean that you should not be careful, but you cannot time the market.

I am not a CPA, so this is not tax advice.

As we mentioned in our post about bonus depreciation for non-real estate professionals, real estate is a government-subsidized investment. Why do I say this? Because if you invest in real estate, the chances are that you will NEVER pay tax on that investment. Almost indefinitely. Some people may say that it’s unfair. However, it is the reality we live in.

Real estate is almost its own ledger. Therefore, all the passive gains and losses generated by your real estate sum up to a single number. For example, if you invest in a big apartment complex, you already have paper losses. Every year you get cash flow, which constitutes capital or passive gains, and you still keep having passive losses on paper.

When you sell the property, you have a substantial gain that you have to pay taxes on. But if you buy another property in the same tax year when you sold the other – you have new capital losses, which will end up wiping out all your gains.

We call it “the rat race of the real estate investing.” By continuously reinvesting higher amounts into real estate, you can indefinitely postpone taxes. Remember that you can never avoid paying taxes altogether, but you can delay paying them.

One important thing to note is that these gains or losses cannot offset your W2 or stocks, especially if you are a non-real estate professional. Read this post to understand how depreciation and tax implications affect real estate professionals.

If you are a real estate professional, your losses can offset even your active income (such as W2). So if you are a software engineer who invests in real estate and your spouse gets a real estate professional status, then all your real estate activity can offset your W2 and other business income as well.

Real-life example: when I sold my first property, I got a substantial gain. To avoid the 10%-15% tax, I put all of that money back into real estate.

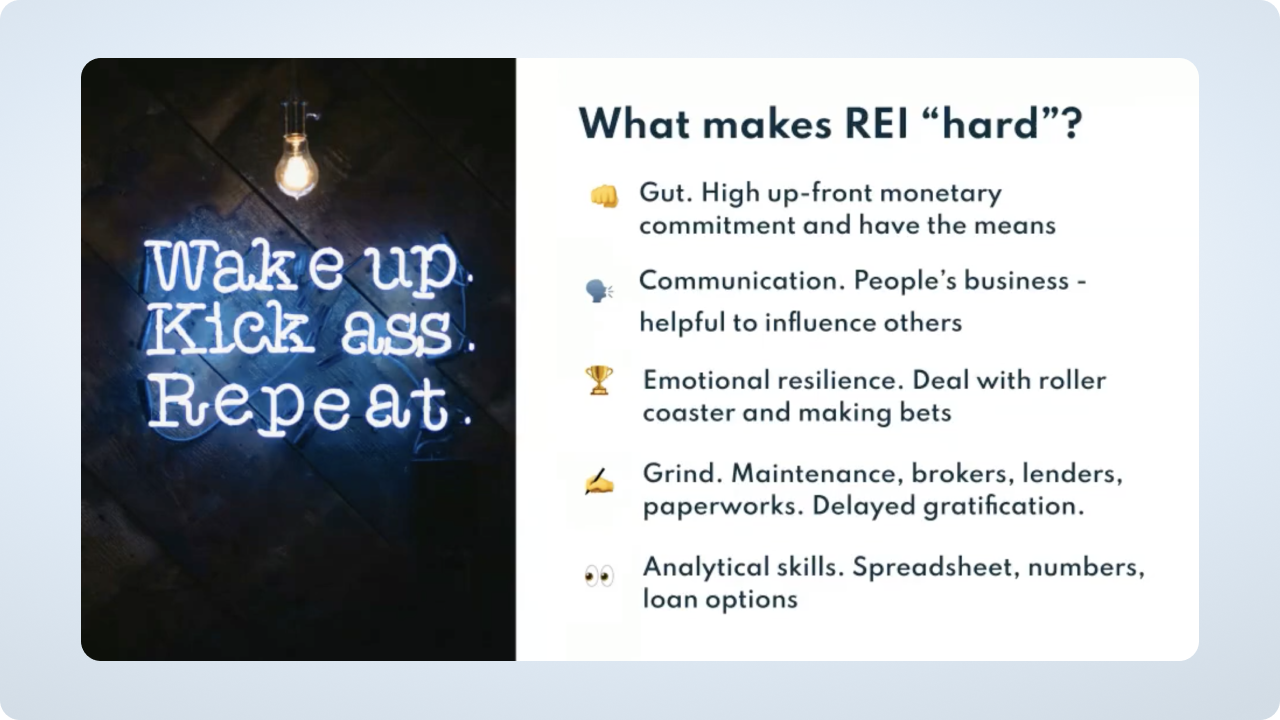

In real estate, it’s essential to have a mindset that is both disciplined and opportunistic. You must be able to roll with the punches as well as pounce on the opportunity. Consequently, there are a few factors that may make REI seem “hard” to some people.

Here are some of them:

You don’t need all of the above attributes to succeed in REI. But if you have two or three of them, developing the others is a question of effort, persistence, and time.

All financial activities involve certain risks. The question is, how significant are those risks? Not all investments are created equal, that’s for sure. Real estate has the lowest downside risk when compared to crypto or stocks. Here are some risks you might encounter when embarking on your journey:

In this article, you learned the basics of real estate investing and how to get started. You can now begin your search for your first house-hacking residence, conduct market analysis, maybe even plan to move to another state or town, and embark on your real estate investing journey. Before you decide on the state you want to invest in, analyze the market by the numbers. Then, based on market conditions, search for an area that can sustain growth in local job markets and develop rental properties.

Real estate is a long-term game of patience, but it attracts many different kinds of investors – from software developers to savvy sales professionals. Real estate is the best business if you want to grow your money and build generational wealth.

You can now put some money down on your first property and begin learning how to be a landlord and a homeowner.

June 24, 2024

May 28, 2024

September 29, 2023